Underinsured Motorist Coverage: What It Means for You in 2026

Learn how underinsured motorist coverage works in 2026. Understand costs, benefits, and examples. Contact Vasquez Law for a free evaluation today.

Published on April 21, 2026

Have questions? Talk to an attorney - free evaluation.

Call 1-844-967-3536Get What Your Injury Is Worth

Free case review, and no fee unless we win.

Underinsured Motorist Coverage: What It Means for You in 2026

Underinsured motorist coverage protects you when you're hit by a driver with insufficient insurance to pay your damages. Especially in Orlando and across Florida and North Carolina, many drivers are underinsured, risking your financial recovery after an accident. This article explains what underinsured motorist coverage means, how it can help you, estimated costs, and steps to take if you're involved in a crash with an underinsured or uninsured driver. Get informed so you can protect yourself and your family in 2026.

Need help with your case? Our experienced attorneys are ready to fight for you. Se Habla Español.

Or call us now: 1-844-967-3536

Quick Answer

Underinsured motorist coverage helps cover your medical bills, lost wages, and damages when the at-fault driver’s insurance is not enough. This coverage can prevent you from paying out of pocket after an accident caused by an underinsured or uninsured driver.

- Protects against drivers with insufficient insurance

- Includes coverage for injuries and property damage

- Costs vary based on location and insurer

- Florida and North Carolina laws differ on requirements

- Contact a personal injury attorney to maximize your claim

Understanding Underinsured Motorist Coverage

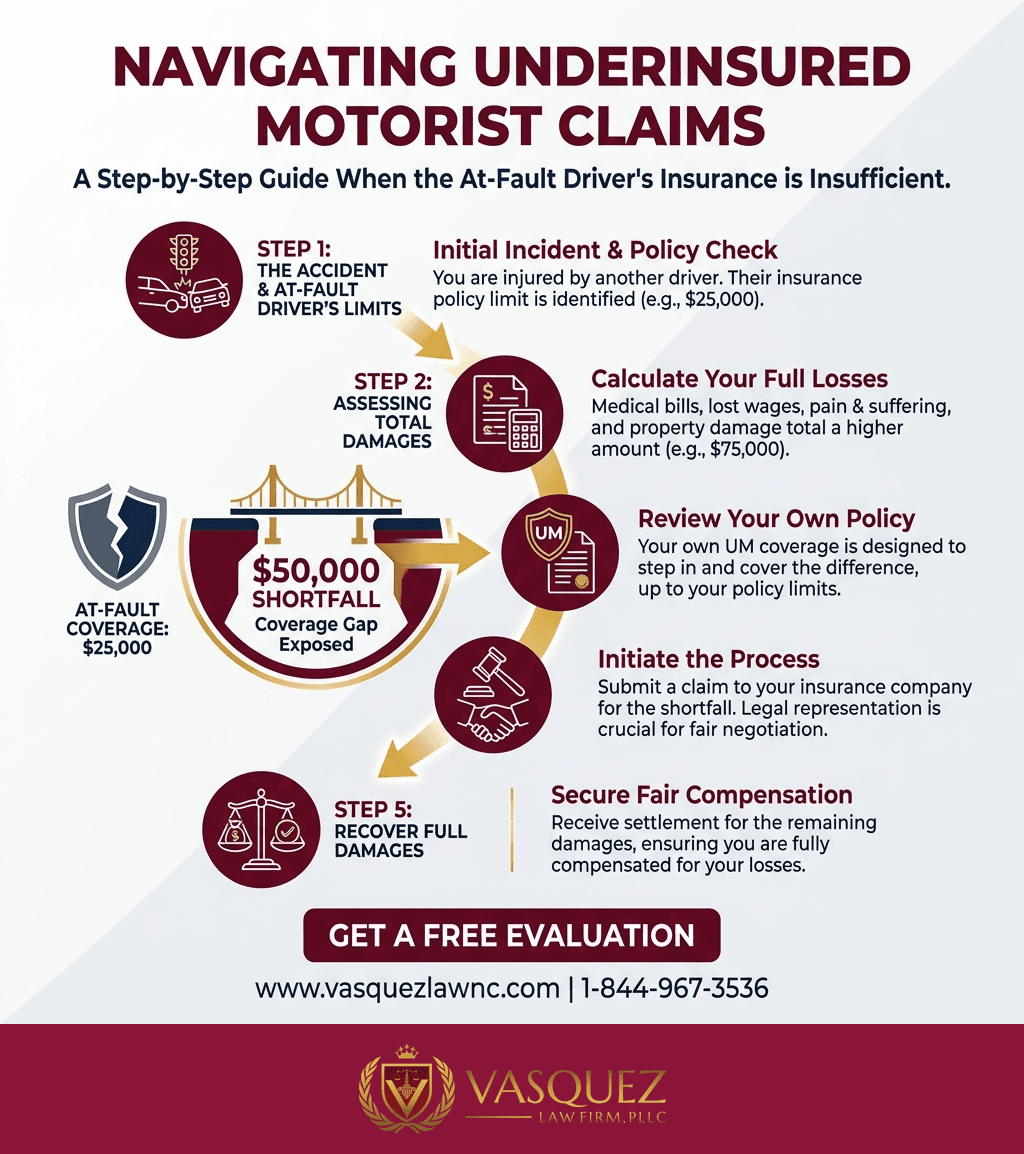

Imagine you are driving in Orlando, and another driver hits you but only carries $25,000 in liability insurance. Your medical bills and property damage reach $75,000. Without underinsured motorist coverage, you would be responsible for the $50,000 shortfall. This type of coverage steps in when the other driver’s insurance isn’t enough to cover your losses.

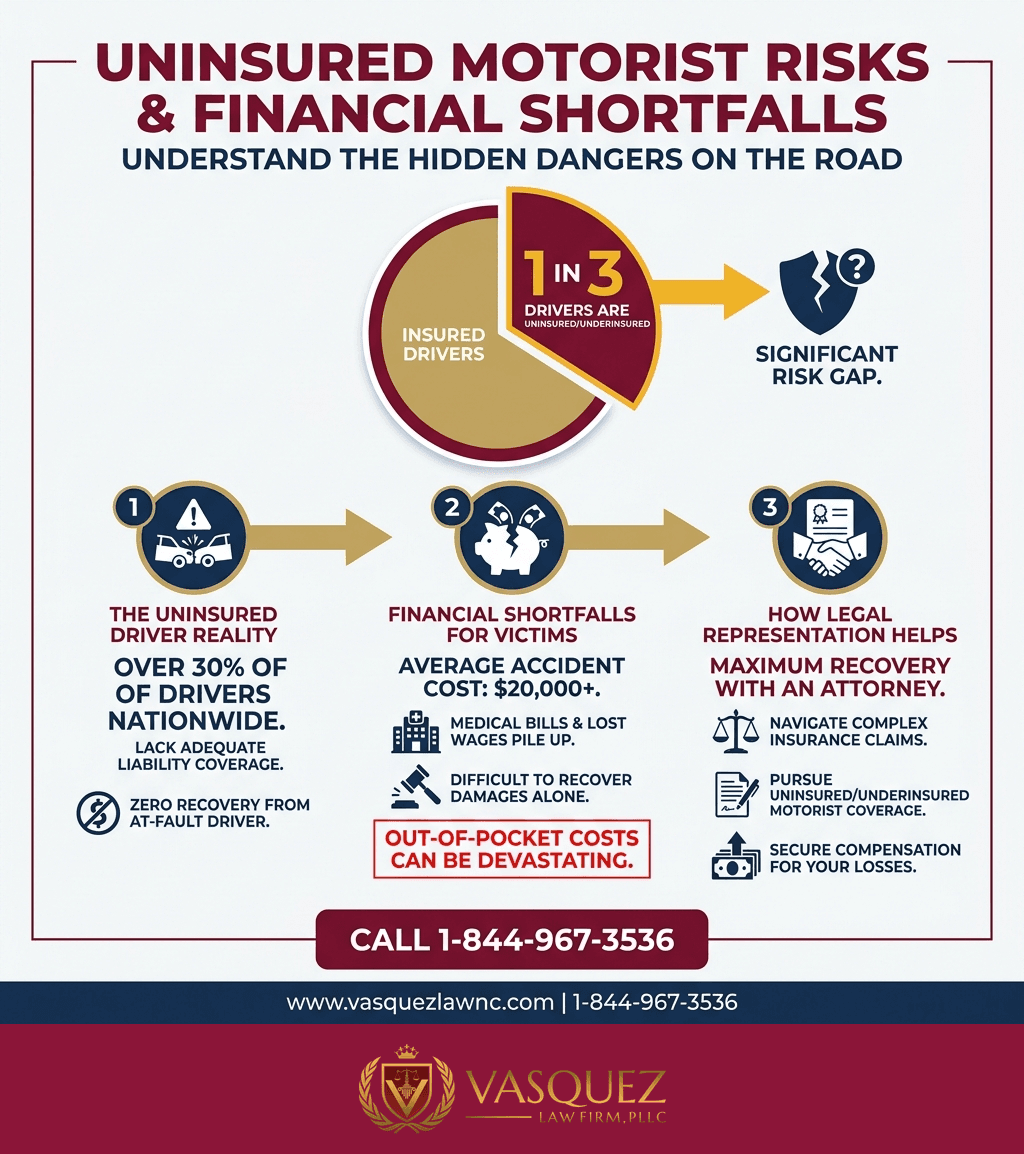

Underinsured motorist coverage safeguards your financial protection after accidents involving drivers who have some, but not adequate, insurance. Many states, including North Carolina and Florida, face a significant number of underinsured motorists, making this coverage vital.

In 2026, insurance experts estimate that approximately 1 in 8 drivers in Florida and North Carolina do not carry sufficient liability limits. This gap exposes victims to unpaid damages and personal financial risk. Adding underinsured motorist coverage helps fill this gap, covering expenses such as medical bills, lost income, and vehicle repairs that exceed the at-fault driver’s policy.

For those interested in personal injury protection in North Carolina, our personal injury services reflect expertise in handling claims involving underinsured motorists. Attorney Vasquez and our legal team have extensive experience dealing with insurance companies and maximizing client recovery.

How Underinsured Motorist Coverage Works

Underinsured motorist coverage activates after your claim against the at-fault driver’s insurer reaches their policy limits. Your insurance then covers the difference up to your underinsured motorist policy limits. This is why selecting adequate coverage limits when purchasing a policy is essential.

Underinsured vs. Uninsured Motorist Coverage

Underinsured motorist coverage applies when the other driver’s insurance is too low. Uninsured motorist coverage applies when the at-fault driver lacks insurance entirely. Many insurance policies combine these coverages as UM/UIM coverage to provide broader protection.

State-Specific Requirements

North Carolina requires insurers to offer uninsured and underinsured motorist coverage, but policyholders may reject it in writing. Florida requires insurers to offer this coverage, and drivers may also reject it in writing, but the state’s high rate of underinsured drivers means accepting this coverage is recommended.

Step-by-Step: How to Use Your Coverage

- Report the accident immediately: Call law enforcement and get a police report documenting the crash.

- Seek medical attention: Even after minor crashes, get examined to document injuries.

- Exchange information: Gather the other driver’s insurance details and contact info.

- Notify your insurer: Report the accident and inform them you may file a claim under underinsured motorist coverage.

- Gather evidence: Take photos of damages, collect witness statements, and save medical records.

- Consult an attorney: Contact an experienced personal injury attorney who understands underinsured motorist claims.

- File your claim: Your attorney can assist with documentation and negotiations with insurance companies.

- Definition and who it protects

- Differences from uninsured motorist coverage

- Why it matters in Florida and North Carolina

Documents and Evidence Checklist

- Police report from the accident

- Medical reports and bills

- Photos of vehicle damage and accident scenes

- Witness contact and statements, if available

- The other driver’s insurance information

- Your insurance policy declarations (showing UM/UIM limits)

- Correspondence with insurance companies

Timeline: What to Expect After an Accident

- First 24-72 hours: Report accident, seek medical care, and notify insurers.

- Within 1-2 weeks: Insurance adjusters contact you to start investigating claims.

- Weeks 2-6: Gather medical documents, damages estimates; negotiate with insurance.

- 1 to 3 months: Settlement discussions or claim denials; possibility to escalate claim.

- 3+ months: Consider litigation with legal counsel if the insurer is uncooperative.

Example Timeline: Orlando Accident in 2026

John was hit by an underinsured driver in Orlando. He reported the crash, saw a doctor the same day, then contacted his insurer. Within 2 weeks, his insurer requested medical records. At 6 weeks, negotiations started. By 3 months, the case settled for $50,000, covering damages above the other driver’s limits.

Costs and Fees: Factors Affecting Coverage Price

- Location: Florida’s higher rates of uninsured drivers may increase premiums.

- Coverage limits: Higher UM/UIM limits raise your premium but increase protection.

- Driving history: Clean records can lower your cost.

- Insurer policies: Different companies price UM/UIM coverage uniquely.

- Existing insurance bundle: Bundling auto with home or other insurance can reduce costs.

Generally, adding underinsured motorist coverage costs 10-15% more than a basic auto insurance policy, but can save thousands in uncovered claims later. In Orlando and surrounding areas of Florida and North Carolina, it is often considered a wise investment.

Common Mistakes and How to Avoid Them

- Rejecting UM/UIM coverage: Fix: Accept the coverage to avoid financial gaps.

- Not reviewing policy limits: Fix: Choose coverage limits that reflect your potential exposure.

- Failing to report an accident promptly: Fix: Notify your insurer and the police immediately after a crash.

- Lack of documentation: Fix: Collect photos, witness contacts, and medical evidence early.

- Ignoring minor injuries: Fix: Get medical exams regardless of how you feel initially.

- Waiting too long to consult a lawyer: Fix: Contact an attorney as soon as possible to protect your rights.

- Settling too quickly: Fix: Understand your case value and seek legal advice before accepting offers.

- Confusing uninsured and underinsured coverage: Fix: Make sure you understand both and confirm they are included in your policy.

- Not knowing state laws: Fix: Learn your state’s specific rules about motorist coverage.

If you only remember one thing: Having underinsured motorist coverage protects you from drivers who don’t carry enough insurance. It safeguards your financial recovery after an accident and is an essential part of your auto insurance in 2026.

North Carolina and Florida Laws and Notes

NC Notes

North Carolina law requires insurers to offer uninsured and underinsured motorist coverage, but drivers may reject it in writing. Limits typically mirror liability limits. The state uses a comparative fault system, which can impact claim amounts. Courts encourage timely claims and accurate documentation. Learn more from the North Carolina Courts.

FL Notes

Florida also mandates offering uninsured and underinsured motorist coverage, but allows a written rejection. Due to Florida’s high traffic accidents and uninsured rates, UM/UIM insurance is critical. Florida follows a no-fault system initially, requiring Personal Injury Protection (PIP) coverage, but UM/UIM provides additional protection when PIP is insufficient. The NCDOT provides data illustrating the high rates of underinsured drivers.

Nationwide Concepts (general only, rules vary)

Underinsured motorist coverage is recognized in most states but not federally mandated. Coverage terms, rejection options, and benefit limits widely vary. Understanding your state’s insurance laws and asking insurers detailed questions is necessary. The National Highway Traffic Safety Administration offers general statistics on uninsured and underinsured motorists in the U.S.

When to Call a Lawyer Immediately

- Serious injury or hospitalization following a crash

- Other driver lacks sufficient or any insurance

- Insurance company denies or undervalues your claim

- Difficulties obtaining the other driver’s insurance information

- Confusion about coverage limits or claim procedures

- Fault is disputed by the other party or insurer

- Settlement offers seem too low or unclear

- Lost wages or long-term disability resulting from the accident

- Property damage exceeds your deductible or expected costs

- Legal deadlines approaching for filing claims or suits

About Vasquez Law Firm

At Vasquez Law Firm, we combine compassion with aggressive representation. Our motto "Yo Peleo" (I Fight) reflects our commitment to standing up for your rights.

- Bilingual Support: Se Habla Español - our team is fully bilingual

- Service Areas: North Carolina, Florida, and nationwide personal injury services

- Experience: Over 15 years helping clients navigate complex legal matters involving motorist coverage

- Results: Thousands of successful cases across personal injury practice areas

Attorney Trust and Experience

Attorney Vasquez holds a Juris Doctor degree and is admitted to practice in both the North Carolina State Bar and Florida Bar. With over 15 years of dedicated legal experience, he has earned a reputation for providing personalized attention and achieving favorable outcomes for clients facing motorist insurance claims and personal injury challenges.

Don't wait to get the help you deserve. Call us now for immediate assistance.

Se Habla Español

Frequently Asked Questions

Is underinsured motorist coverage worth having?

Yes. Underinsured motorist coverage protects you when an at-fault driver does not have enough insurance to pay for damages or injuries. It’s especially important in Florida and North Carolina where many drivers carry minimum insurance, helping you avoid expensive medical bills and vehicle repair costs that might otherwise come out of your pocket.

Who pays when you are hit by an uninsured or underinsured driver?

If you have uninsured/underinsured motorist coverage, your own insurance policy will cover the expenses up to your coverage limits. Without it, you may have to pay out of pocket or attempt to sue the at-fault driver, which may be difficult if they lack assets or insurance.

What does $100,000/$300,000/$100,000 mean in car insurance?

These numbers describe liability coverage limits: $100,000 per person for bodily injury, $300,000 total per accident for bodily injury, and $100,000 for property damage. They represent the maximum amounts an insurance company will pay in each category after an accident.

Do I need uninsured motorist coverage if I have collision and comprehensive insurance?

Collision and comprehensive insurance cover damage to your own vehicle, but they don’t pay for your injuries or other damages caused by uninsured drivers. Underinsured motorist coverage is necessary to protect against expenses that other insurance does not cover.

What factors affect the cost of underinsured motorist coverage?

Costs depend on your location, driving history, coverage limits, and your insurer’s pricing. In Florida and North Carolina, this coverage adds a reasonable premium to your insurance but can greatly reduce your financial risk after an accident.

Can I sue an underinsured driver if I have underinsured motorist coverage?

Yes, you can pursue legal action if damages exceed your insurance limits. However, the insurance coverage can reduce the need for litigation by paying up to your policy limit, and a lawyer can help assess when suing the driver is appropriate.

How does Florida law treat underinsured motorist coverage?

Florida requires insurers to offer this coverage, but drivers may reject it in writing. Due to a high rate of underinsurance, most experts recommend accepting this coverage to protect yourself from heavy out-of-pocket expenses should an accident occur.

What steps should I take after an accident with an underinsured driver?

Document the accident with photos and police reports, get medical care, exchange insurance information, notify your insurer promptly, and consult an experienced personal injury attorney to help maximize your claim under your underinsured motorist coverage.

Sources and References

- North Carolina Courts

- North Carolina Department of Transportation

- National Highway Traffic Safety Administration

Take the first step toward justice today. Our team is standing by to help you.

Start Your Free Evaluation Now

Call us: 1-844-967-3536

Se Habla Español - Estamos aquí para ayudarle.

William Vasquez

Founder & CEO, Vasquez Law Firm, PLLC

William Vasquez is the founder and CEO of Vasquez Law Firm, PLLC, a results-driven firm specializing in immigration, criminal defense, personal injury, and workers' compensation. A U.S. Air Force veteran and recipient of the Joint Service Achievement Medal, William is dedicated to fiercely fighting for his clients' rights.

Related Legal Services

Need legal help? Learn more about learn about our personal injury practice, or contact us for a free evaluation.

You can also visit personal injury lawyers across North Carolina for more information.