What Banks Checking Citizenship Verification Means for Immigrants in 2026

Understand how citizenship verification impacts bank accounts and immigration in 2026. Get expert insights & contact Vasquez Law for a free consultation today.

Published on February 26, 2026

Have questions? Talk to an attorney - free evaluation.

Call 1-844-967-3536Free Tool

Check Your USCIS Case Status Now

Enter your receipt number - get the official USCIS status in English or Spanish. No registration.

What Banks Checking Citizenship Verification Means for Immigrants in 2026

The topic of citizenship verification banks and its implications for individuals, especially immigrants, is a complex and evolving area of law. As of 2026, discussions around potential new requirements for financial institutions to verify the citizenship or immigration status of their customers continue to generate significant concern and confusion. This guide aims to clarify the current landscape, what existing regulations require, and how proposed changes could impact your financial life and immigration journey. Understanding these nuances is crucial for protecting your assets and ensuring compliance. Vasquez Law Firm is dedicated to providing up-to-date information and robust legal representation for those navigating these challenges in North Carolina, Florida, and nationwide.

Need help understanding your rights regarding citizenship verification and banking? Our experienced attorneys are ready to fight for you. Se Habla Español.

Schedule Your Free Consultation

Or call us now: 1-844-967-3536

Quick Answer: Citizenship Verification for Banks in 2026

As of 2026, banks are primarily required to verify a customer's identity, not necessarily their citizenship, under federal regulations like the Bank Secrecy Act and the USA PATRIOT Act. While a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) is often requested, specific citizenship verification banks mandates for all account holders are not currently in widespread effect, though proposals have surfaced periodically.

- Banks must verify identity to combat financial crime.

- SSN or ITIN typically required for account opening.

- No universal mandate for banks to verify citizenship status.

- Proposals for stricter citizenship verification have faced legal and practical hurdles.

- Immigrants often use ITINs to open accounts legally.

- Rules primarily focus on identity and tax compliance, not immigration status.

Understanding Current Banking Regulations and Citizenship Verification

Financial institutions in the United States operate under strict federal regulations designed to prevent money laundering, terrorist financing, and other illicit activities. Key among these are the Bank Secrecy Act (BSA) and the USA PATRIOT Act. These laws mandate that banks implement Customer Identification Programs (CIPs) to verify the identity of anyone opening an account. This typically involves collecting information such as name, date of birth, address, and an identification number, like a Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN).

It is important to distinguish between identity verification and citizenship verification. While banks must confirm who you are, they are not generally required to confirm your citizenship status for basic account opening. Non-citizens, including undocumented immigrants, can legally open bank accounts using an ITIN, which is issued by the IRS for tax purposes. This allows individuals to participate in the financial system, pay taxes, and avoid carrying large amounts of cash, which is a security risk.

Despite the current framework, there have been political discussions and proposals over the years to impose more stringent citizenship verification requirements on banks. These discussions often stem from broader immigration policy debates. However, such proposals face significant practical challenges, including the immense burden on financial institutions and potential legal challenges regarding discrimination and privacy. Understanding the current legal landscape is vital for individuals concerned about how citizenship verification banks could impact their access to financial services.

Bank Secrecy Act and USA PATRIOT Act

The Bank Secrecy Act (BSA), enacted in 1970, is a cornerstone of U.S. anti-money laundering (AML) efforts. It requires financial institutions to assist U.S. government agencies in detecting and preventing money laundering. This includes filing reports of suspicious activity and currency transactions over certain thresholds. The USA PATRIOT Act, passed in response to the September 11th attacks, significantly expanded the BSA's reach, requiring banks to establish robust Customer Identification Programs (CIPs) to verify the identity of account holders.

Under a CIP, banks must collect specific identifying information from customers, such as name, date of birth, address, and an identification number. For U.S. persons, this is typically an SSN. For non-U.S. persons, it can be an ITIN or other government-issued identification. The primary goal is to ensure the person opening the account is who they claim to be, not necessarily to verify their citizenship status. These measures are critical for national security and financial integrity, but they do not impose a blanket citizenship verification requirement on banks. FinCEN (Financial Crimes Enforcement Network) provides further guidance on BSA compliance.

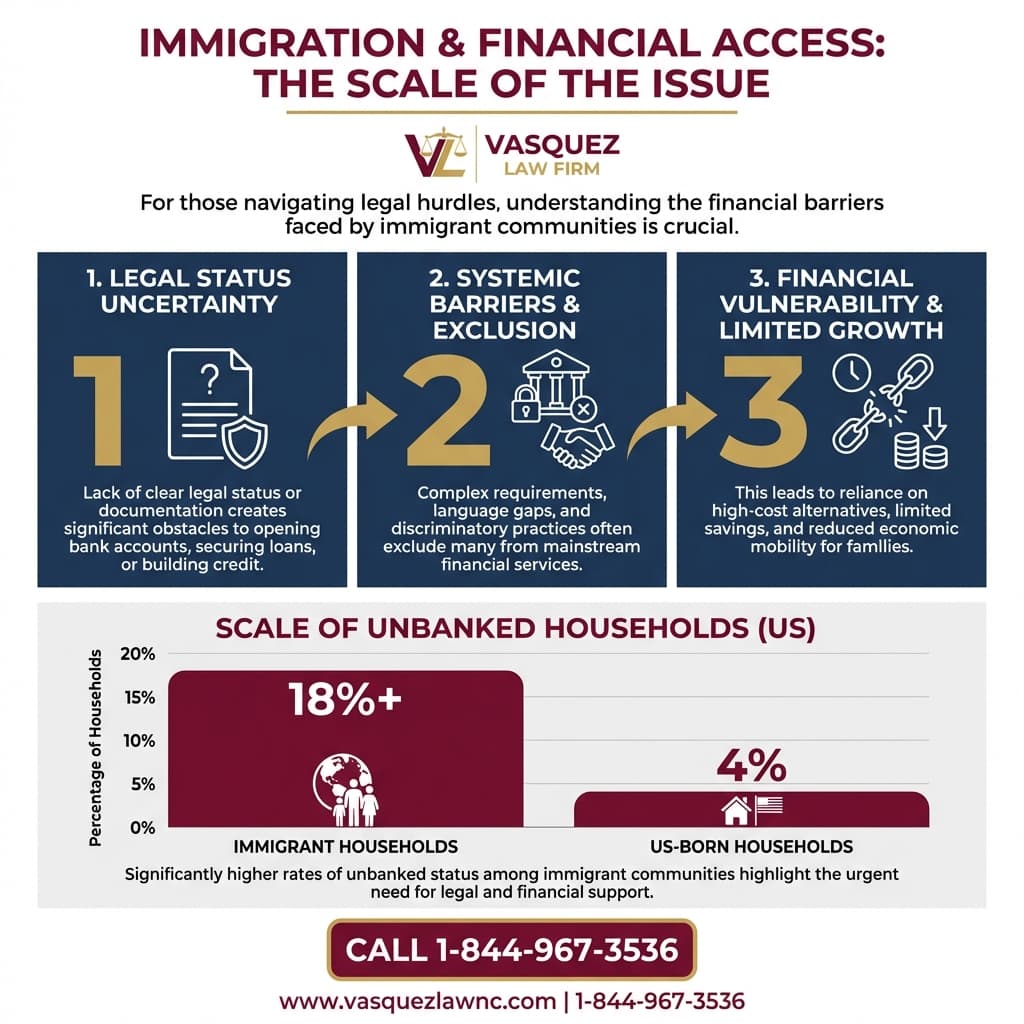

How Citizenship Status Impacts Financial Services Access

While U.S. citizenship is not strictly required to open a bank account, an individual's immigration status can influence access to certain financial products and services. For example, some specialized loans, credit cards, or investment accounts might have stricter eligibility criteria that favor U.S. citizens or lawful permanent residents. However, basic checking and savings accounts are generally accessible to most individuals residing in the U.S., provided they meet identity verification requirements and have a valid tax identification number.

The Individual Taxpayer Identification Number (ITIN) plays a crucial role for many non-citizens. Issued by the IRS to individuals who are required to have a U.S. taxpayer identification number but do not have, and are not eligible to obtain, an SSN, the ITIN allows individuals to comply with U.S. tax laws and access financial services. This means that individuals without U.S. citizenship can often integrate into the financial system, pay taxes, and build credit history, which is essential for economic stability and future opportunities. Our firm assists clients in Orlando, Florida, and across North Carolina with immigration matters that often intersect with financial planning.

It is important for individuals, particularly Dreamers and other immigrants, to understand their rights and the legal avenues available to them when seeking financial services. Fear of discrimination or confusion about regulations should not prevent eligible individuals from accessing necessary banking services. Vasquez Law Firm can provide guidance on navigating these issues, ensuring that your rights are protected and that you can access the financial tools you need. We stay abreast of all immigration law changes in 2026 that might affect financial access.

ITINs and Access to Banking

The Individual Taxpayer Identification Number (ITIN) is a tax processing number issued by the U.S. Internal Revenue Service (IRS) to individuals who are required to have a U.S. taxpayer identification number but who do not have, and are not eligible to obtain, a Social Security Number (SSN). ITINs are crucial for non-citizens, including undocumented immigrants, who have tax obligations in the U.S. Beyond tax compliance, ITINs are widely accepted by banks and other financial institutions as a valid form of identification number for opening checking accounts, savings accounts, and obtaining other financial services.

The acceptance of ITINs by banks is a testament to the federal government's policy of allowing all residents to participate in the financial system, regardless of their immigration status, for purposes of tax collection and financial stability. This practice helps prevent individuals from operating solely in cash, reducing risks associated with theft and increasing financial transparency. If you are a non-citizen seeking to open a bank account, presenting a valid ITIN along with other forms of identification, such as a passport or a foreign national identification card, should generally suffice. For more information, you can consult the IRS website on ITIN applications.

Potential Changes and Their Impact on Citizenship Verification Banks

While no sweeping federal mandate for universal citizenship verification by banks is currently in place as of 2026, the political landscape is always subject to change. Proposals have emerged in the past, often during shifts in presidential administrations, suggesting that banks might be required to undertake more rigorous checks on customers' immigration status. Such changes, if implemented, could have profound effects on millions of individuals, particularly those in immigrant communities.

The implications of stricter citizenship verification banks requirements could include increased difficulty for non-citizens to open or maintain bank accounts, potential closures of existing accounts, and a push towards a cash-only economy for many vulnerable populations. This could exacerbate financial exclusion, make it harder for individuals to save money, pay bills, and participate in the mainstream economy, and create significant compliance burdens for financial institutions. Any such policy would likely face immediate legal challenges from civil rights organizations and banking industry groups, arguing against discrimination and impracticality.

It's crucial for individuals and businesses to stay informed about any proposed legislation or regulatory changes that could affect financial access. Vasquez Law Firm closely monitors these developments to provide timely advice and representation. Our immigration attorneys, serving clients in North Carolina and Florida, are prepared to advocate for your rights and help you understand how potential policy shifts might impact your situation. We believe in proactive legal counsel to mitigate risks and ensure continued financial stability for all our clients.

Past Proposals and Their Fate

Historically, various administrations have explored ideas for enhanced citizenship verification by banks. For instance, during the Trump administration, there were reports of discussions about potentially requiring banks to verify the citizenship status of all account holders. These proposals were often framed as measures to enforce immigration laws more broadly. However, such initiatives have typically not moved beyond the discussion phase or have encountered significant pushback.

The reasons for their limited success are multifaceted. Banking industry groups have consistently highlighted the immense operational costs and logistical complexities of implementing such a system. Civil liberties advocates have raised concerns about potential discrimination and privacy violations. Furthermore, the existing legal framework, which focuses on identity and tax compliance through SSNs and ITINs, already provides a functional system for financial oversight. The legal and practical hurdles for implementing a universal citizenship verification requirement remain substantial, making it a challenging policy to enact. This history underscores the importance of legal vigilance against policies that could harm immigrant communities.

Steps to Protect Your Financial Accounts and Immigration Status

Given the ongoing discussions around citizenship verification banks, taking proactive steps to safeguard your financial accounts and ensure compliance with immigration laws is paramount. Here's a guide to what you can do:

- Maintain Accurate Records: Keep all your immigration documents, tax identification numbers (SSN/ITIN), and bank statements organized and up-to-date. This includes passports, visas, Green Cards, and any notices from USCIS or the IRS.

- Understand Your Bank's Policies: Be familiar with your bank's specific identity verification policies. While federal law sets minimums, individual banks may have additional requirements.

- Use Official Identification: Always use valid, government-issued identification when dealing with financial institutions. For non-citizens, this might include a foreign passport, a consular identification card, or a U.S. visa.

- Consult with an Immigration Attorney: If you have concerns about your immigration status or how potential policy changes could affect your banking, speak with a qualified immigration lawyer. They can provide personalized advice and help you understand your rights.

- Stay Informed: Keep abreast of legislative and regulatory changes related to immigration and financial services. Reliable legal news sources and organizations can provide valuable updates.

- Avoid Cash-Only Operations: Where possible, utilize formal banking services. Relying solely on cash can be risky and makes it harder to prove financial stability or income if needed for immigration applications.

- Report Discrimination: If you believe you have been denied banking services due to discrimination based on your national origin or immigration status, document the incident and consider reporting it to relevant authorities or legal advocacy groups.

Taking these steps can help you maintain financial stability and navigate any potential challenges related to citizenship verification banks. Attorney Vasquez and our team are here to provide comprehensive support for your immigration and related financial concerns. We offer services in Orlando, Florida, and throughout North Carolina.

Documents and Evidence Checklist for Banking

When opening a bank account or if your bank requests updated information, having the correct documents ready can streamline the process and help alleviate concerns about citizenship verification banks. Here is a checklist of commonly accepted documents:

- Primary Identification:

- Valid unexpired U.S. driver's license or state ID card

- Valid unexpired foreign passport (often with a U.S. visa if applicable)

- U.S. Permanent Resident Card (Green Card)

- Employment Authorization Document (EAD card)

- Taxpayer Identification Number:

- Social Security Card (SSN)

- Individual Taxpayer Identification Number (ITIN) assignment letter from the IRS

- Proof of Address (if not on ID):

- Utility bill (electricity, water, gas)

- Lease agreement or mortgage statement

- Bank statement or credit card statement (from another institution)

- Other Supporting Documents (as requested):

- Birth certificate (U.S. or foreign)

- Consular identification card

- Any other government-issued identification

Always bring original documents, as banks typically require them for verification purposes. If you are unsure about what documents your bank requires, it is best to contact them directly or consult with an attorney.

Don't face your legal challenges alone. Our team is here to help you every step of the way.

Call today: 1-844-967-3536 | Se Habla Español

Common Mistakes to Avoid with Financial and Immigration Matters

Navigating the intersection of financial services and immigration law can be fraught with potential pitfalls. Avoiding these common mistakes is crucial for protecting your financial stability and immigration status, especially concerning citizenship verification banks:

- Ignoring Bank Communications:

Mistake: Disregarding notices or requests from your bank for updated information or identity verification. Fix: Always respond promptly to bank inquiries. If you don't understand a request, seek clarification from the bank or consult legal counsel.

- Using False or Inaccurate Information:

Mistake: Providing incorrect or fraudulent information to a bank, even inadvertently, which can lead to account closure and legal repercussions. Fix: Always be truthful and accurate in all your financial dealings. Fraudulent activity can severely jeopardize your immigration standing.

- Operating Exclusively in Cash:

Mistake: Avoiding banks entirely due to fear or misinformation, leading to financial insecurity and difficulty proving income or residency. Fix: Understand that most immigrants can legally access banking services. Using banks provides security, builds financial history, and simplifies tax compliance.

- Not Understanding ITIN Benefits:

Mistake: Failing to apply for an ITIN if you're eligible, which can limit financial access and tax compliance. Fix: If you have U.S. tax obligations but no SSN, apply for an ITIN. It's a legitimate tool for financial inclusion.

- Confusing Identity Verification with Citizenship Verification:

Mistake: Assuming banks are requiring citizenship proof when they are only conducting standard identity checks. Fix: Know the difference. Banks primarily verify identity. If you're asked for citizenship, clarify the specific requirement and its legal basis.

- Lack of Legal Counsel for Complex Situations:

Mistake: Attempting to navigate complex banking or immigration issues without professional legal advice. Fix: For any significant concerns about your immigration status, financial access, or potential policy changes, consult an experienced immigration attorney. Attorney Vasquez offers dedicated legal support.

- Failing to Update Immigration Status:

Mistake: Not updating your immigration status with relevant authorities, which can create discrepancies in official records. Fix: Ensure USCIS and other agencies have your most current immigration status. This helps maintain consistency across all your official records.

If you only remember one thing: Always be truthful with financial institutions and seek legal guidance from an immigration attorney if you have any doubts about your rights or obligations concerning citizenship verification banks.

NC, FL, and Nationwide Notes on Citizenship Verification

The issue of citizenship verification banks primarily falls under federal jurisdiction, as banking regulations (like the BSA and USA PATRIOT Act) and immigration laws (Title 8 of the U.S. Code) are federal matters. This means that the core requirements for identity verification in banking apply uniformly across all states, including North Carolina and Florida.

North Carolina Notes

In North Carolina, financial institutions adhere to federal guidelines for identity verification. Immigrants in North Carolina, including those in Orlando, can generally open bank accounts using valid identification and an SSN or ITIN. There are no specific state laws in North Carolina that impose additional citizenship verification requirements on banks beyond federal mandates. Local advocacy groups and legal aid organizations in North Carolina often provide resources to immigrant communities regarding financial access and rights. Our firm, serving clients across North Carolina, ensures that individuals understand their federal rights within the state's context.

Florida Notes

Similarly, in Florida, banks follow federal regulations regarding customer identification. Immigrants in Florida, including in cities like Orlando, can access banking services with appropriate identification and a tax ID. Florida does not have state-specific laws that add extra layers of citizenship verification for bank accounts beyond what federal law requires. However, the political climate around immigration can sometimes lead to state-level discussions or proposals, though these rarely alter federal banking requirements. Vasquez Law Firm is well-versed in both federal and Florida-specific nuances impacting immigration and financial matters for our clients in Orlando and other Florida communities.

Nationwide Concepts (General Only, Rules Vary)

Across the United States, the principle remains that identity verification, not necessarily citizenship verification, is the primary focus for banks. The federal framework ensures a baseline level of access to financial services for all residents, regardless of immigration status, provided they can meet identity and tax compliance requirements. While state-specific initiatives might arise, they typically cannot supersede federal banking laws. It's a nationwide practice that ITINs facilitate banking for those without SSNs. However, the legal landscape is dynamic, and staying informed about any federal legislative changes is critical for anyone concerned about citizenship verification banks.

When to Call an Immigration Lawyer Now

The complexities surrounding citizenship verification banks, coupled with evolving immigration policies, mean that legal guidance can be invaluable. You should consider contacting an experienced immigration attorney if:

- Your bank requests proof of citizenship specifically, beyond standard identity verification.

- Your bank account is frozen or closed due to questions about your immigration status.

- You are denied the ability to open a bank account despite providing valid identification and an ITIN.

- You fear discrimination from a financial institution based on your national origin or perceived immigration status.

- You have received a notice from a government agency (like USCIS or IRS) that impacts your financial accounts.

- There are new federal or state proposals for citizenship verification banks that concern you.

- You are a Dreamer or an individual with DACA status facing new banking challenges.

- You need help obtaining an ITIN or understanding its implications for banking.

- You are applying for immigration benefits and need to demonstrate financial stability.

- You have general concerns about how your immigration status intersects with your financial rights.

Don't wait until a problem escalates. Early intervention by a knowledgeable attorney can often prevent more serious issues. The Vasquez Law Firm is ready to provide the aggressive and compassionate representation you deserve. Contact us today for a free consultation to discuss your specific situation.

About Vasquez Law Firm

At Vasquez Law Firm, we combine compassion with aggressive representation. Our motto "Yo Peleo" (I Fight) reflects our commitment to standing up for your rights. We understand the unique challenges faced by immigrant communities and are dedicated to providing clear, effective legal solutions.

- Bilingual Support: Se Habla Español - our team is fully bilingual, ensuring clear communication and understanding.

- Service Areas: We proudly serve clients across North Carolina and Florida, with nationwide immigration services. Our Orlando office is ready to assist you.

- Experience: With over 15 years of dedicated experience, Attorney Vasquez has a proven track record in immigration, personal injury, workers' compensation, and criminal defense.

- Results: We are committed to achieving favorable outcomes, guiding thousands of clients through complex legal matters with personalized attention.

Attorney Trust and Experience

Attorney Vasquez holds a Juris Doctor degree and is admitted to practice in both the North Carolina State Bar and Florida Bar. With over 15 years of dedicated legal experience, he has built a reputation for providing personalized attention and achieving favorable outcomes for his clients. His deep understanding of immigration law, including its intersection with financial regulations, makes him a trusted advocate for individuals and families navigating these critical issues. He is committed to fighting for justice and ensuring that every client receives the highest quality legal representation.

Frequently Asked Questions About Citizenship Verification Banks

Can I open a bank account in the U.S. without being a citizen?

Yes, non-citizens can legally open bank accounts in the U.S. Banks are primarily required to verify your identity, not necessarily your citizenship status. You will typically need a valid form of identification, such as a foreign passport, and a tax identification number, like a Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN). Many banks are accustomed to serving non-citizens who reside in the U.S.

What is an ITIN and how does it help with banking?

An Individual Taxpayer Identification Number (ITIN) is a tax processing number issued by the IRS to individuals who are required to have a U.S. taxpayer identification number but do not have, and are not eligible to obtain, an SSN. Banks accept ITINs for identity verification purposes, allowing non-citizens to open accounts, pay taxes, and engage in the financial system legally. It's a key tool for financial inclusion.

Are banks required to report my immigration status to the government?

Generally, banks are not required to report a customer's immigration status. Their primary obligations under laws like the Bank Secrecy Act and USA PATRIOT Act are to verify identity and report suspicious financial activities to prevent money laundering and terrorism financing. While they collect identifying information, this is for financial compliance, not immigration enforcement. Specific citizenship verification banks mandates for reporting immigration status are not currently widespread.

What if my bank asks for proof of citizenship?

If your bank specifically asks for proof of U.S. citizenship beyond standard identity verification, clarify the reason for the request. While rare for basic accounts, some specialized financial products might have stricter requirements. If you feel you are being discriminated against or are unsure of your rights, it is advisable to consult with an immigration attorney to understand the legality and implications of such a request.

Can my bank account be closed if my immigration status changes?

A change in immigration status alone should not automatically lead to the closure of a legally opened bank account. Banks typically require updated identification if your existing documents expire or if there's a significant change in your identity information. However, if there are discrepancies or issues with your identity verification that raise red flags for the bank's compliance team, your account could be flagged. Maintaining accurate and current information with your bank is crucial.

What documents do I need to open a bank account as a non-citizen?

As a non-citizen, you typically need a valid unexpired foreign passport, sometimes with a U.S. visa, or a U.S. Permanent Resident Card (Green Card) or Employment Authorization Document (EAD). You will also need a tax identification number, either an SSN or an ITIN. Additionally, proof of address, such as a utility bill, may be required. Always bring original documents for verification.

Are there any state laws in NC or FL that require citizenship verification for banking?

No, neither North Carolina nor Florida currently have state-specific laws that impose additional citizenship verification requirements on banks beyond federal mandates. Banking regulations, including customer identification programs, are primarily governed by federal laws like the Bank Secrecy Act and the USA PATRIOT Act, which apply nationwide. Therefore, the requirements for opening bank accounts are generally consistent across both states for citizens and non-citizens alike.

How can Vasquez Law Firm help with banking and immigration concerns?

Vasquez Law Firm provides comprehensive legal guidance for individuals navigating the intersection of immigration and financial services. We can help you understand your rights regarding citizenship verification banks, assist with ITIN applications, advise on potential policy changes, and represent you if you face discrimination or account issues. Our attorneys offer personalized advice to ensure your financial stability and compliance with immigration laws in North Carolina, Florida, and nationwide.

What is the USA PATRIOT Act's role in bank identity checks?

The USA PATRIOT Act significantly expanded the Bank Secrecy Act, requiring financial institutions to establish robust Customer Identification Programs (CIPs). These programs mandate that banks collect and verify identifying information from customers to prevent money laundering and terrorist financing. While the act enhances identity checks, its primary focus is on ensuring a customer's true identity, not their citizenship status, allowing for the use of ITINs by non-citizens.

Could a future administration force banks to verify citizenship?

While past administrations have explored the idea of requiring banks to verify citizenship, such proposals have faced significant legal and practical challenges. Implementing such a mandate would require new federal legislation or extensive regulatory changes, which would likely be met with strong opposition from civil rights groups and the banking industry. The current system prioritizes identity and tax compliance, making a universal citizenship verification mandate a complex and contentious policy to enact.

Sources and References

- U.S. Citizenship and Immigration Services (USCIS)

- Executive Office for Immigration Review (EOIR)

- Internal Revenue Service (IRS) - Apply for an ITIN

- Financial Crimes Enforcement Network (FinCEN) - Bank Secrecy Act

Ready to take the next step? Contact Vasquez Law Firm today for a free, confidential consultation. We're committed to fighting for your rights and achieving the best possible outcome for your case.

Start Your Free Consultation Now

Call us: 1-844-967-3536

Se Habla Español - Estamos aquí para ayudarle.

William Vasquez

Founder & CEO, Vasquez Law Firm, PLLC

William Vasquez is the founder and CEO of Vasquez Law Firm, PLLC, a results-driven firm specializing in immigration, criminal defense, personal injury, and workers' compensation. A U.S. Air Force veteran and recipient of the Joint Service Achievement Medal, William is dedicated to fiercely fighting for his clients' rights.

Related Legal Services

Need legal help? Learn more about our immigration legal services, or contact us for a free evaluation.

You can also visit North Carolina immigration lawyers for more information.